The Basics of Benchmarking

Updated January 2, 2015 by Matt H. Evans

Benchmarking provides several benefits, including better understanding of the competition, better performance, and objective evaluations of performance based on real examples. One way to leverage benchmarking is to develop cost data and cost the process or activity that is being benchmarked. This provides a "perfect world" view of the activity since all costs not related to the activity are removed; especially any abnormal or unusual costs. This view of costs is becoming increasingly important since management must understand costs under a perfect scenario if the company expects to compete in the global marketplace. Additionally, management and investors are starting to push for perfection because of programs like Six Sigma.

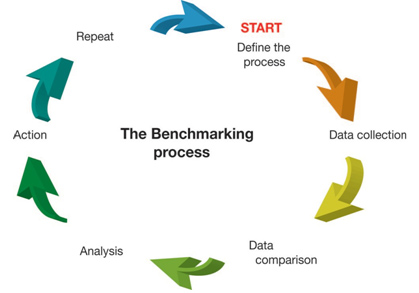

The basic process for setting up benchmarks will usually consist of:

- 1) Identify and understand the function or process that needs to be benchmarked. Determine end-user requirements for benchmarking.

- 2) Organize a benchmarking team for design and implementation of benchmarking.

- 3) Understand the process and related activities. You need to make sure have comparability; otherwise you may end up comparing apples to oranges. The goal is to find relevant benchmarks for improving performance.

- 4) Research and gather "best in class" performance data. This may require interviews, research, analysis and other tasks. For small companies on a tight budget, outside services may have to supply the benchmark data. Larger companies will develop their own in-house benchmark data.

- 5) Analyze the data and determine performance gaps between your company and "best in class" benchmarks. Identify the causes for the gaps and establish future attainable performance.

- 6) Obtain senior management support for benchmarking. Finalize the benchmark standards and assess their impacts.

- 7) Apply the benchmarks and continuously update the benchmark data.

The best types of benchmarks focus on critical functions or processes in the business, such as production efficiency or customer service. A solid understanding of the function or process is critical to finding the right benchmark. You are trying to pull out the right performance data for external benchmarking. External benchmarking is considerably more difficult than internal benchmarking.

Finding financial related benchmark data is not too difficult. Financial benchmarks are widely available from service bureaus, market reports, financial reports, and published surveys. Financial benchmarking can help you determine the costs of a process or activity based on perfect cost conditions. The key to benchmarking is to make sure you have a good comparison. Once you have this out of the way, you should find the appropriate benchmark and allow the benchmark to help guide your performance. Always remember to benchmark against "best in class" and not averages. You are not interested in average performance; you want to move towards best in class.

Written by: Matt H. Evans, CPA, CMA, CFM | Email: matt@exinfm.com | Phone: 1-877-807-8756

Written by: Matt H. Evans, CPA, CMA, CFM | Email: matt@exinfm.com | Phone: 1-877-807-8756